Talking Points:

- Last week of the month brings a heavy US calendar.

- Wednesday headlines week with FOMC and RBNZ.

- Keep an eye on inflation data at the end of the week.

Volatility reared its ugly head this past week, but those that were agile enough saw opportunity among the disarray. Indeed, trading conditions reminiscent of 2011 and 2012 returned: fear drove trading, as evidenced by the decoupling of the AUDUSD from US Treasuries, in which the safe haven risk-on/risk-off dichotomy reemerged. The fact that a dense calendar has descended upon the markets during a period of heightened volatility increases the need for any trader to respect the rules of risk management.

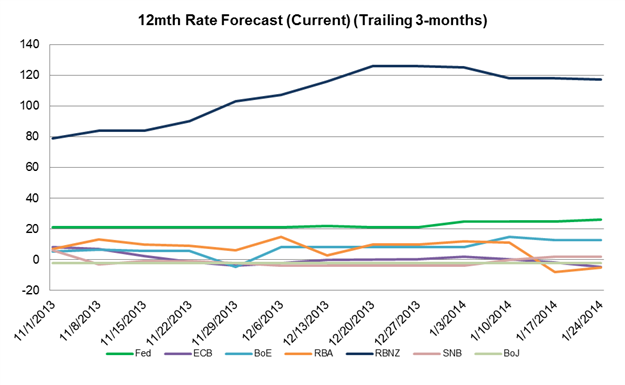

If there ever was a week that encompassed a plethora of various economic indicators, it was this one: 4Q’13 US GDP, 4Q’13 UK GDP, German Unemployment, Euro-Zone and Japanese CPI. Plus, the Federal Reserve and the Reserve Bank of New Zealand meet on Wednesday. Coincidentally, these are two of the major central banks that are becoming incrementally more hawkish at each meeting – meaning the tail end of the week should bring even more excitement to the currency markets.

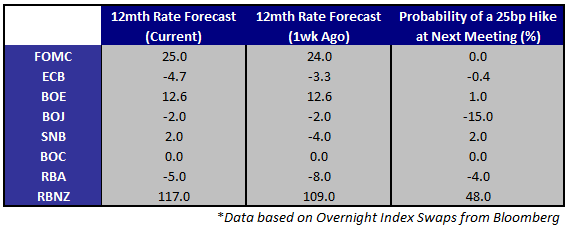

Rate Hike Probabilities / Basis-Points Expectations

See the DailyFX Calendar for a full list, timetable, and consensus forecasts for upcoming economic indicators. See all of this week’s “high”importance events.

01/28 Tuesday // 09:30 GMT: GBP Gross Domestic Product (4Q A)

Prospects continue to brighten for the UK economy and this has led to heavy buying in GBP-crosses over the past few months. If this GDP print meets estimates, it will be the highest yearly rate of growth since 2008. Market participants continue to push further Pound strength as speculation of an earlier than expected rate hike continue to remain the talk of the street regarding the Bank of England. Barring a miss, the British Pound remains one of our favorite bullish fundamentals plays for 2014.

Survey: +0.7% (q/q), +2.8% (y/y)

Prior: +0.8% (q/q), +1.9% (y/y)

The key pairs to watch are EURGBP and GBPJPY.

01/28 Tuesday // 13:30 GMT: USD Durable Goods Orders (DEC) // 15:00 GMT: Consumer Confidence (JAN)

These will be the last major data prints out of the US moving into the FOMC rate decision on Wednesday. The Durable Goods Orders print for November has already been revised slightly lower by a tenth of a percent, but a December survey of +1.8% remains relatively strong. Consumer Confidence is expected to pullback to 78.0, but the print has remained above 70 since May and in the absence of any upsetting print, USD-crosses are likely to consolidate ahead of the Fed.

Durable Goods

Survey: +1.8% (m/m)

Prior: +3.4% (m/m)

Consumer Confidence

Survey: 78.0

Prior: 78.1

The key pairs to watch are EURUSD and USDJPY.

01/29 Wednesday // 19:00 GMT: USD Federal Open Market Committee Rate Decision

With no FOMC meeting for the month of February, this meeting and the Minutes in two weeks will set consensus on the Fed until March. Market participants are expecting a $10B taper, split evenly between Treasury and MBS purchases. Although some may be skeptical of a reduction in asset purchases this time around in the context of the last NFP release, Fed members have stated that one weak NFP print is nothing to overreact to or build consensus around – neither is emerging market turmoil.

Survey: main rate unch at 0.25%, QE3 cut by $10B to $65B/month

Prior: main rate unch at 0.25%, QE3 cut by $10B to $65B/month (unexpected cut)

The key pairs to watch are EURUSD and USDJPY.

01/29Wednesday // 20:00 GMT: NZD Reserve Bank of New Zealand Rate Decision

The RBNZ is easily the most hawkish major central bank presently, with a +48% chance of a 25-bps rate hike at its upcoming meeting. Local financial institutions are more hawkish, with ANZ Bank calling for a surprise rate hike at the meeting. No doubt, rate expectations have been building: there are now +117.0-bps priced in over the next 12-months. In the event of no rate hike – a hold is the consensus according to the Bloomberg News forecast – we expect the commentary to retain an overall hawkish tone nonetheless, even if Governor Graeme Wheeler expresses his displeasure with the New Zealand Dollar’s elevated exchange rate.

Survey: main rate unch at 2.50%

Prior: main rate unch at 2.50%

The key pairs to watch are AUDNZD and NZDUSD.

01/30 Thursday // 13:30 GMT: USD Gross Domestic Product (4Q A) (Annualized)

Surveys are lower for 4Q’13 GDP estimates after last month’s blowout print that sent US yields to three month highs. USD moves to the upside at the release were short lived though as market participants pulled back positioning ahead of Friday’s NFP release. This time around we will have more clarification with the FOMC just passed and the release of the January NFP report not until the following week, so moves here in the US Dollar have an opportunity be more defined by this release.

Survey: +3.2%

Prior: +4.1%

The key pairs to watch are EURUSD and USDJPY.

--- Written by Christopher Vecchio, Currency Analyst and Gregory Marks, DailyFX Research

To contact Christopher Vecchio, e-mail cvecchio@dailyfx.com

Follow him on Twitter at @CVecchioFX

To be added to Christopher’s e-mail distribution list, please fill out this form

original source