|

|

| This week's gainers and losers |

| Gainers: Williams-Sonoma (+20%): The holding company which oversees several home furnishings chains in the United States hit new record highs after announcing better-than-expected annual results for the year ended January. These were accompanied by the inevitable $1 billion share buyback program, which is considerable given the company's capitalization ($18.3 billion). MicroStrategy Incorporated (-17%): Shares of the analytics and business intelligence company rose after it filed to raise $500 million in a convertible debt offering, with a view to purchasing more bitcoin. This comes a few days after the company closed on an $800 million convertible debt raise. Southern Copper (+17%): Copper prices rose sharply this week, after Chinese smelters announced production cuts, due to a tighter-than-expected raw materials market. As a result, copper prices in Shanghai reached their highest level in three years, while prices in London reached their highest level in 10 months. Oracle (+12%): The software company's share price hit new records this week, after reporting buoyant prospects thanks to its exposure to the cloud computing market in general, and artificial intelligence in particular. Oracle also announced during the week the addition of generative artificial intelligence functions to its enterprise software range. Losers: Southwest Airlines (-18%): The airline has revised downwards its forecasts for the number of aircraft it expects to receive from its supplier Boeing. The carrier is expected to receive only 46 737-8 family aircraft this year, instead of the 79 anticipated. Bad news that will weigh on results. Adobe (-11%): Adobe Systems Incorporated's forecasts disappointed despite solid revenue growth. Its stock plummeted, despite reporting an 11% increase in revenue for the first quarter. The decline in profit, coupled with the company's projection of a sales growth slowdown to 9% in the second quarter, was too much for investors, who believed in the company's AI prospects. Enphase (-16%) : The share price suffered again this week, in the absence of any specific information. According to our sources, Enphase could be collateral damage from the efficiency of Tesla's latest home battery system, the PW3, which incorporates an inverter and makes traditional inverter-equipped systems like Enphase's more expensive. Dollar Tree (-15%): The American discounter disappointed the market with weak quarterly results. The group was also forced to close 970 of its Family Dollar stores, caught between retail giants like Walmart and aggressive new entrants such as the Chinese e-commerce platform Temu. Dollar Tree has taken considerable write-downs, which put a strain on its accounts. |

|

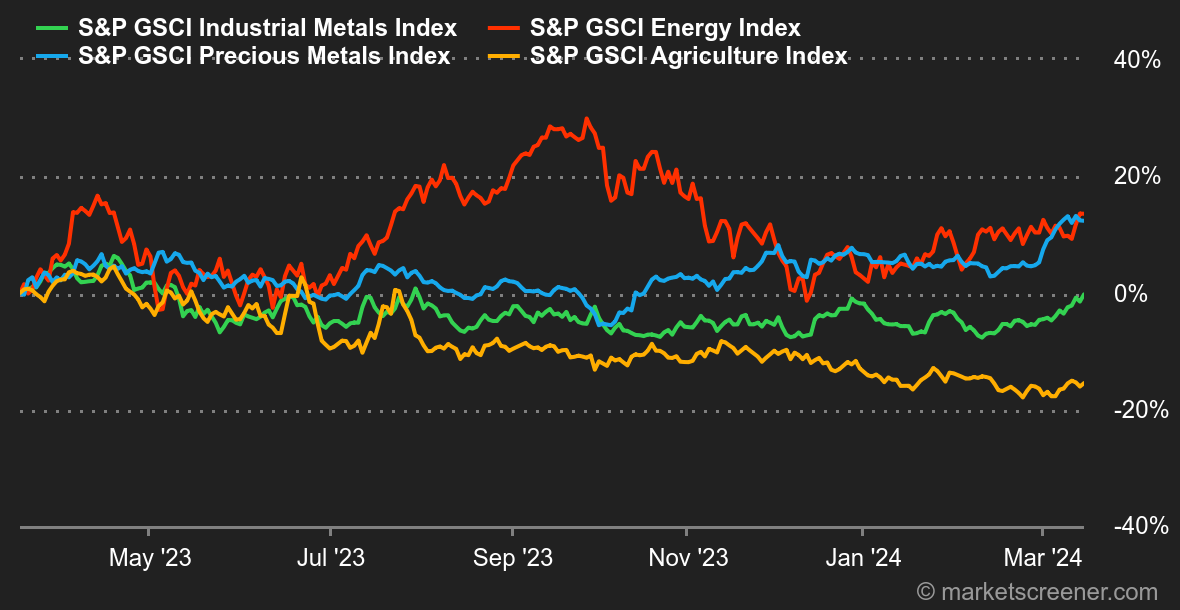

| Commodities |

| Energy: The mood on the oil markets has changed this week, with traders realizing that the market is not all that well supplied. The International Energy Agency has thrown a spanner in the works, announcing in its latest monthly report that the market could be in deficit this year. The Agency revised upwards its demand growth forecasts, while at the same time adjusting downwards the dynamics of world supply due to OPEC+ policy. Against this backdrop, geopolitical friction remains high in Ukraine, which has struck oil installations in Russia, as well as in the Middle East, particularly in the Red Sea. Finally, weekly US inventories posted a surprise decline this week, the first since the end of January. In terms of prices, Brent crude is trading higher at around USD 85, while WTI is trading at around USD 80.80. Metals: Copper continues to perform well in London, approaching the USD 9,000 per metric ton mark. The reason for this upturn is to be found on the supply side, as China plans to ease up on its copper production. Indeed, China's largest smelters have agreed to reduce their output. Still on the industrial metals front, aluminum stabilized at USD 2,200 and zinc advanced to USD 2,520. In gold, the precious metal took a breather after two strong weeks, trading at USD 2160. Bond yields are rising again, overshadowing the ounce of gold. Agricultural products: In Chicago, grain prices are struggling to recover. Bushels of corn and wheat are trading at around 435 and 530 cents respectively. |

|

| Macroeconomics |

| Atmosphere: The market is overpriced. Intoxicated by the rise in equity markets and promises of future rate cuts, we thought inflation was out of the picture for good. Well, here it is, playing spoilsport and reminding investors of their good fortune. First of all, CPI Core (US core inflation) came in slightly above forecasts at +3.8% y/y. Admittedly, no one took this into account at the time. Unfortunately, the second Kiss Cool effect came two days later with the PPI (US producer prices). On an annual basis, it showed a rise of 1.60%, against a forecast of 1.2%, while on a monthly basis, it showed +0.60% against +0.30% expected. It's hard to turn a blind eye here. What's more, the yield on the US 10-year bond, which finally held up well on its 4.07% support, has risen to 4.3%. Crypto: Bitcoin (BTC) is down 1.40% this week around the $68,000 mark, after hitting a new all-time high of $73,830 on Thursday. Bitcoin Spot ETFs are still fuelling the rise, with a record day of net inflows into these exchange products on Wednesday. No less than $1.05 billion flowed into ETFs on a single day. Overall, the ten Bitcoin Spot ETFs have $57.86 billion in assets under management, representing 4.16% of all bitcoins in circulation. Meanwhile, ether (ETH) is down 4% this week. On the other hand, the cryptocurrency has yet to regain its all-time high of $4,800, reached in November 2021, unlike bitcoin, which has already broken its own record. Many are eagerly awaiting an Ethereum Spot ETF so that the asset too can benefit from Wall Street's fresh money. But for the time being, this is not on the agenda of the US regulator. |

|

|

| Things to read this week | ||||||

|

|

*The weekly movements of indexes and stocks displayed on the dashboard are related to the period ranging from the open on Monday to the sending time of this newsletter on Friday. The weekly movements of commodities, precious metals and currencies displayed on the dashboard are related to a 7-day rolling period from Friday to Friday, until the sending time of this newsletter. These assets continue to quote on weekends. |